[ad_1]

The Avenue Supermarts Ltd stock is back to square one. Investors were thrilled when the company, which runs the DMart supermarket chain of stores, said earlier this month that its December quarter (Q3FY25) standalone year-on-year revenue growth came in at 17.5%. The better-than-expected show meant Avenue’s shares closed almost 12% higher on 3 January.

However, the optimism was short-lived due to subdued broader markets and worries about how the margin would pan out. Margin fears came true. Q3 results revealed Avenue’s operating margin fell at a sharper-than-expected pace. Avenue’s shares dropped by around 5% on Monday to ₹3,507.45 apiece, below the levels seen on 2 January.

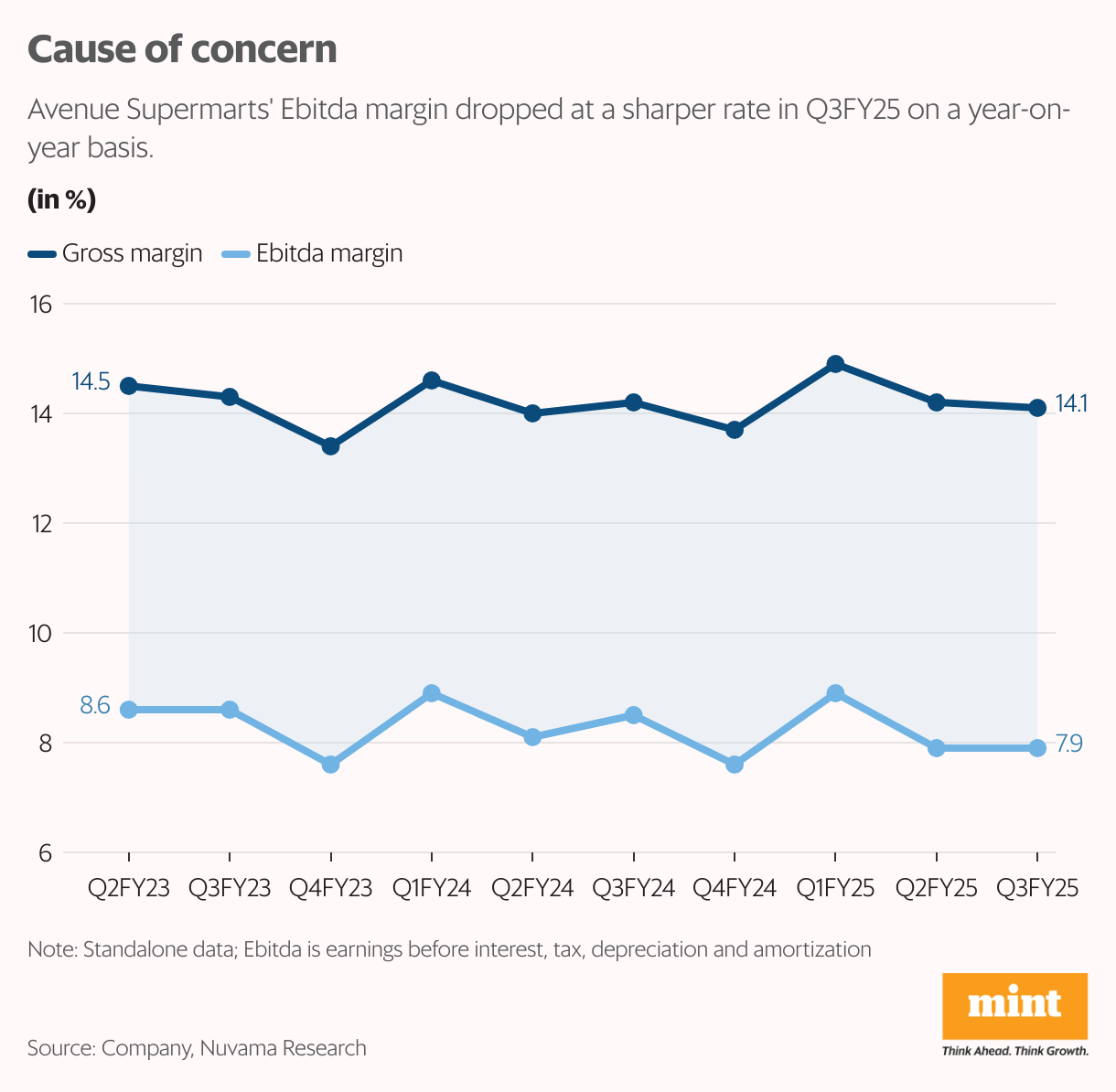

The company’s Ebitda (earnings before interest, taxes, depreciation, and amortization) margin contracted 53 basis points (bps) year-on-year to 7.9% in the quarter. One basis point is one-hundredth of a percentage point.

The upshot is that Ebitda growth was at a slower pace than revenue growth at 10% to ₹1,235 crore. To be sure, Avenue’s gross margin was not a problem in Q3, but the main culprits that hurt Ebitda performance were faster pace of growth in staff costs and other expenses.

Avenue has said it continues to see increased intensity in discounting in the FMCG category and the consequent impact on high turnover per square foot in stores in metro towns. Even so, the impact in Q3 was relatively lower compared to Q2, according to Avenue.

Following Q3, some have cut their earnings estimates. “Post the 3QFY25 performance and factoring in competition from online groceries impacting growth and margins, we cut our Ebitda estimate by 5%-12% over FY25-27E,” said an Antique Stock Broking report on 11 January. “Further, the CEO’s exit could impact the short-term performance. Hence, we cut our target multiple from 45x EV/Ebitda to 40x,” it added.

Impact of leadership change

A part of the weakness in Avenue’s shares could be attributed to the management changes, too. Avenue has said Neville Noronha will step down as managing director and chief executive when his current term ends in January 2026. Noronha has had a notable 20-year-plus stint at Avenue.

The company’s board has appointed Anshul Asawa as the CEO designate, effective 15 March. He is expected to take over as the MD and CEO on 1 February 2026. Asawa is serving as country head of Unilever in Thailand and general manager of the home-care business unit in Greater Asia.

Analysts from Kotak Institutional Equities believe the key expectations from Asawa would be (1) fixing the issue of store additions, (2) addressing the DMart Ready growth problem amid competition from quick commerce and (3) significantly improving digitization, including customer data collection and mining.

In the nine months ended December, Avenue added 22 stores, taking the total count to 387. Store additions are expected to increase in Q4. A pick-up in store additions remains a key growth driver for the company.

“While we too expect most things to continue, we hope for an acceleration in store adds, a key investor worry recently; comprehensive steps to combat rise in competition will also improve long-term visibility; finally, better disclosure, transparency and more investor engagement is also on our mind,” said Jefferies India’s analysts in a report dated 12 January.

In the backdrop of heightening competition, Avenue’s shares are down as much as 36% from their 52-week highs in September. The stock trades at 66 times estimated earnings for FY26, showed Bloomberg data. Valuations are not particularly comforting. Investor focus should be on how Avenue navigates rising competition and delivers on growth and margin.

[ad_2]

Live Mint